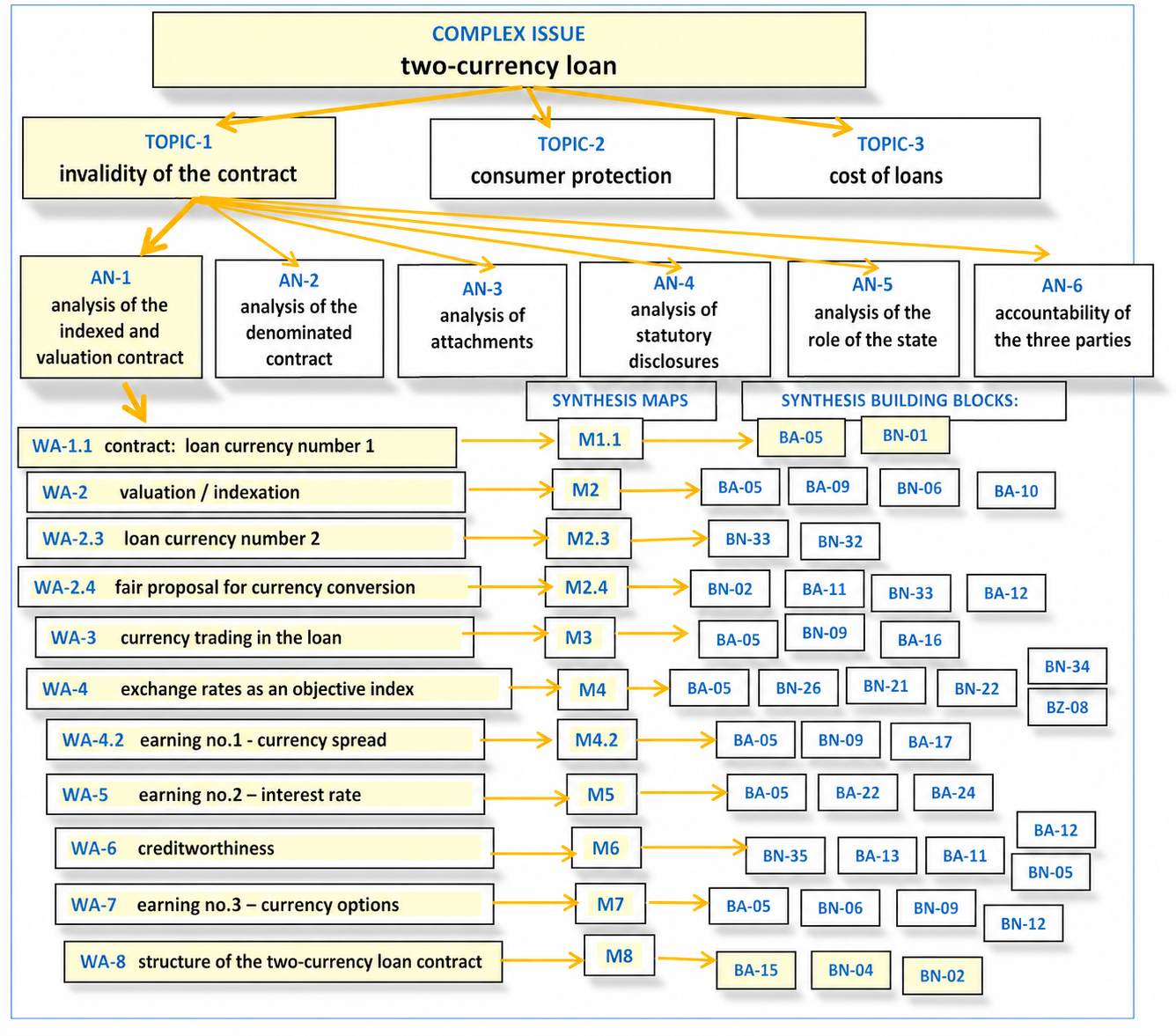

AI-1

ANALYSIS of the text of a dual-currency loan agreement (valorized and indexed)

Introductory explanation:

Here I present an analysis of the TEXT OF THE LOAN AGREEMENT, which no one has yet made available to public opinion.

I will analyse the meanings of the individual paragraphs, above all from the perspective of the provisions concerning the price of the loan, and I will check what effects the signing of the agreement produces.

I will also consider the structure of the wording. I will try to determine whether all the arrangements resulting from the agreement are understandable to the average consumer at first glance, or only after expert analysis.

Indexed, valorized and denominated loan agreements — unlike PLN loans or classic foreign-currency loans, which are taken out and repaid in the same currency — provide in their wording that

the amount of the disbursed loan and the amount of the repaid debt are in different currencies.

This means that at the moment the agreement is signed, they do not clearly specify — in the currency in which the loan is taken out —

the amount of principal to be repaid.

A detailed analysis of the content of the agreement, with no missing logical links, is necessary in order to verify whether its provisions are correct and fair.

For convenience, on this page I will use the term dual-currency loans whenever it does not matter which exact type of loan is at issue — indexed, valorized or denominated.

In carrying out the analysis, I will isolate the key issues in this agreement.

I will do this in eleven points, but only two of them, WA-1.1 and WA-8, contain all the necessary studies.

The remaining issues are shown only in outline.

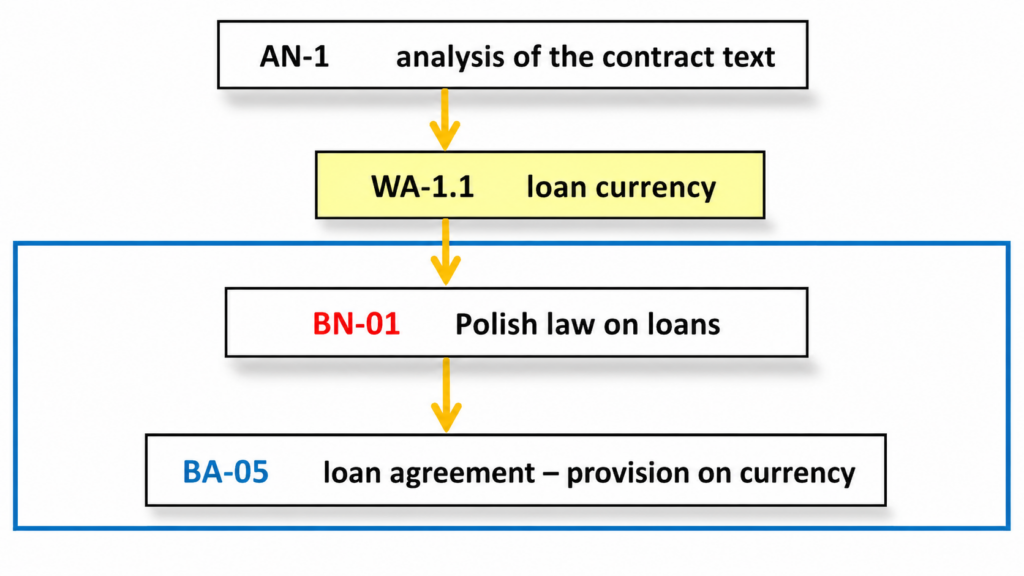

WA-1.1 loan currency number 1

Under Banking Law, the currency of the loan must be clearly specified, and all arrangements and financial settlements should take place in that very currency.

→ so what is the formal currency of the pseudo-Swiss-franc agreement?

CONCLUSION

The currency of the loan is undoubtedly PLN.

Moreover, it should be noted that Polish law did not provide for the possibility of entering two currencies into a loan agreement.

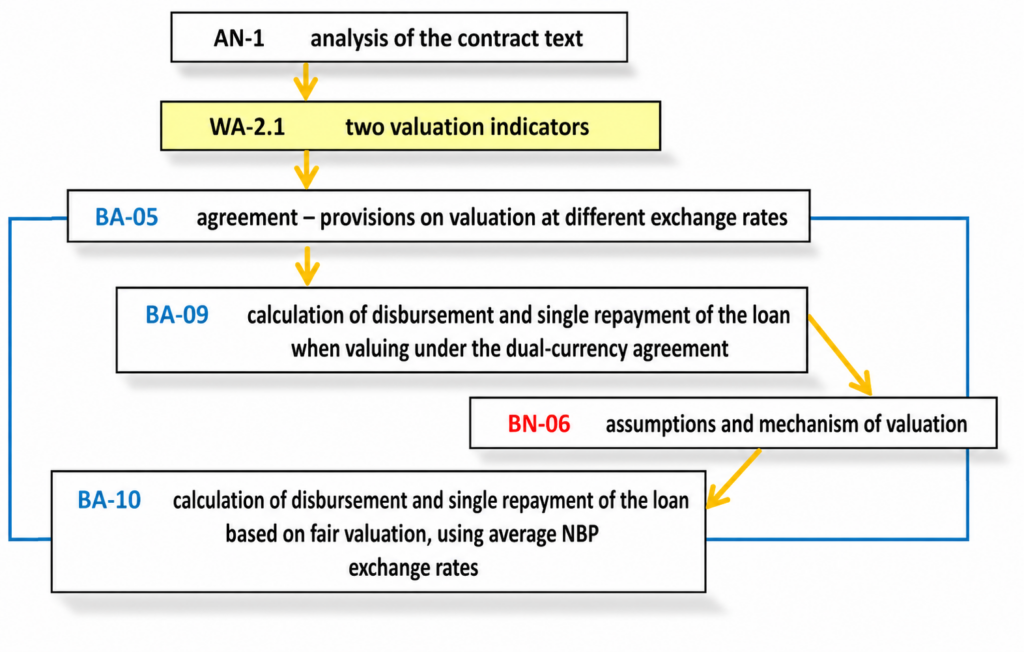

WA-2 valorization (indexation)

Valorization is a legal principle which states that, in the event of a change in the purchasing power of money after an obligation has arisen, the creditor should receive the economic equivalent (higher or lower) of the claim as of the moment it arose. Valorization assumes that monetary performances are intended to provide the creditor with the same economic value as the claim had at the moment it arose, which means that between the arising of the debt and its repayment, time must pass in order for one to speak of a change in the value of the debt!

Valorization is always dependent on some indicator — in this case, the exchange rate of a foreign currency.

However, a dual-currency loan agreement assumes the adoption of two valorization/indexation measures, i.e. two different exchange rates — buying and selling. In such an understanding of “valorization”, the passage of time is not needed for the debt to change its value. Already at the moment the loan agreement is signed, the loan amount is different from the amount of the debt created for repayment, because the buying and selling rates of a currency are always different. One party to the agreement loses on both operations, and the other gains on both — this gives rise to two issues:

WA-2.1 → Is the use of two valorization indicators consistent with the assumptions of valorization?

Can the valorization/indexation of a loan have a different indicator for each party to the agreement — one at disbursement and another at repayment?

CONCLUSION

The concept of valorization or indexation used in a dual-currency agreement has little to do with their common understanding.

Two indicators cannot be used for valorization/indexation — one when converting from PLN to CHF and another in the opposite direction. It is also certain that valorization or indexation is not the conversion of Polish zlotys into Swiss francs. A PLN loan valorized/indexed to a foreign currency remains a PLN loan.

It would be equally possible to valorize/index to the price of gold or the price of wheat — and then, according to the logic of most Polish economists, borrowers should be able to repay the loan in gold bars or sacks of wheat?

Unfortunately, many people (including lawyers appearing on behalf of borrowers) call loans indexed to the Swiss franc “Swiss-franc loans”, and in this way the boundary between a loan actually granted in Swiss francs and one merely indexed to the franc has been blurred. If there were no such difference, there would be no indexed/valorized loans, only foreign-currency loans.

Why were the transactions contained in the dual-currency agreement given such names?

… Certainly because it sounds good, but was there some other — substantive — reason?

Of course there was, but bankers did not want to advertise it, because it could have been regarded as inconsistent with the applicable regulations.

WA-2.2 → Is loan disbursement connected with currency trading?

This is a somewhat separate issue, which is why I discuss it in a separate point [→ WA 3]

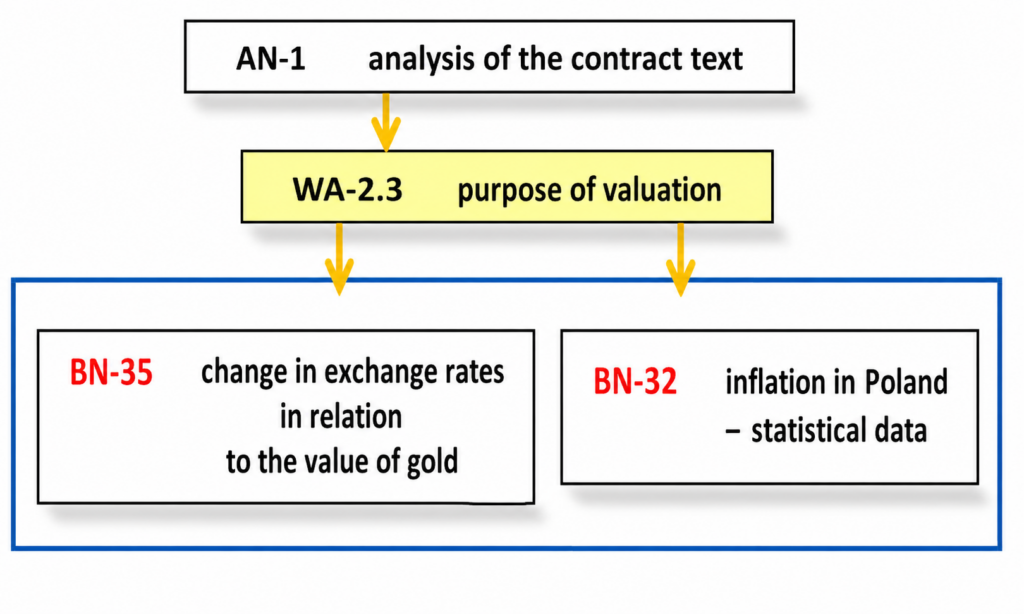

WA-2.3 loan currency number 2

The purpose of properly understood valorization is to provide the creditor with the same economic value as the claim had at the moment it arose.

→ Can the exchange rate of a single currency be a measure of the change in the purchasing power of another currency?

CONCLUSION

Changes in the prices of consumer goods, real estate and services in Poland are not unequivocally linked to the strengthening or weakening of the CHF exchange rate, or of another foreign currency, against the PLN.

A clause on valorization or indexation allows one → to introduce a second currency into the loan agreement.

The purpose of this so-called valorization is … a dual-currency agreement.

This is neither a PLN loan nor a foreign-currency loan, but a new type of dual-currency loan.

Inflation in our country is not directly linked to the change in the exchange rate of any single foreign currency. Therefore, the so-called valorization in dual-currency agreements was not intended to provide the creditor with the equivalent of the zlotys that were lent, but with the equivalent of Swiss francs, which were not lent, but into which the bank converted the zlotys at the time of loan disbursement.

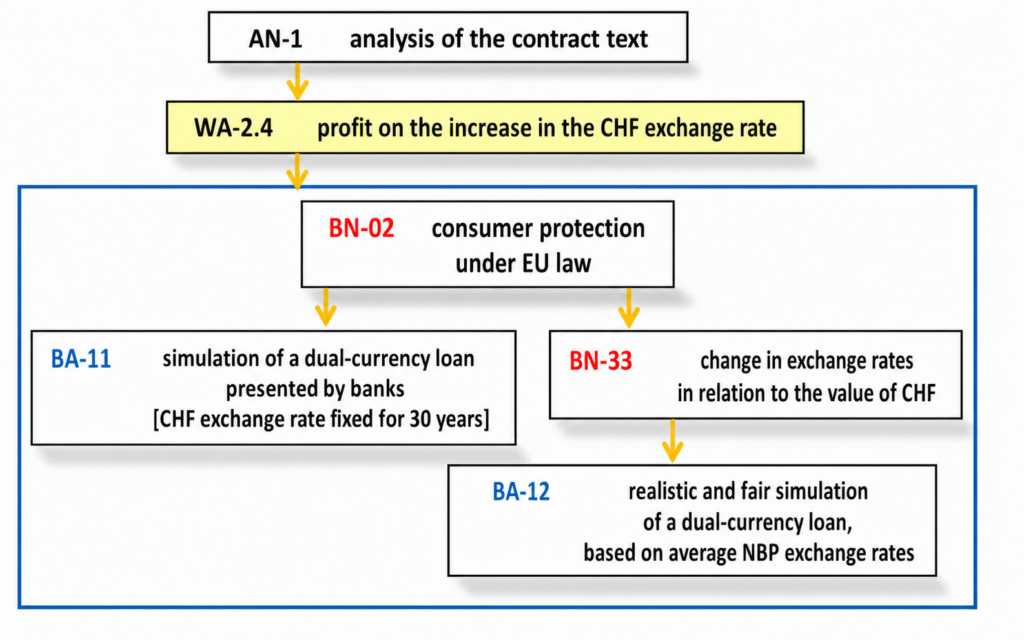

WA-2.4 fair currency-conversion offer

The purpose of the so-called “valorization” was not valorization, but solely profit from the increase in the CHF exchange rate — but did the bankers do this fairly?

→ Did they clearly tell the borrower: “we are lending you zlotys, but we will convert them into CHF, and over the last 30 years the CHF exchange rate has behaved vis-à-vis other currencies as follows…” → show the exchange-rate changes on charts “CHF interest rates are lower than PLN rates, but there is the following exchange-rate risk” → show a loan simulation based on a realistic change in CHF rates, and only then ask the question → “do you want to borrow zlotys, but repay the debt to us after conversion into Swiss francs at the average rate determined by the National Bank of Poland?”

CONCLUSION

The loan-repayment simulations prepared by bankers were unrealistically understated (the foreign-currency exchange rate remains unchanged for thirty years), which creates the impression that the exchange-rate change has no significance here.

A fair offer should take realistic exchange-rate changes into account and should be based on the rate of an entity independent of both transaction parties, e.g. the average NBP rate, whereas it was based on the exchange rate set by the bank-lender.

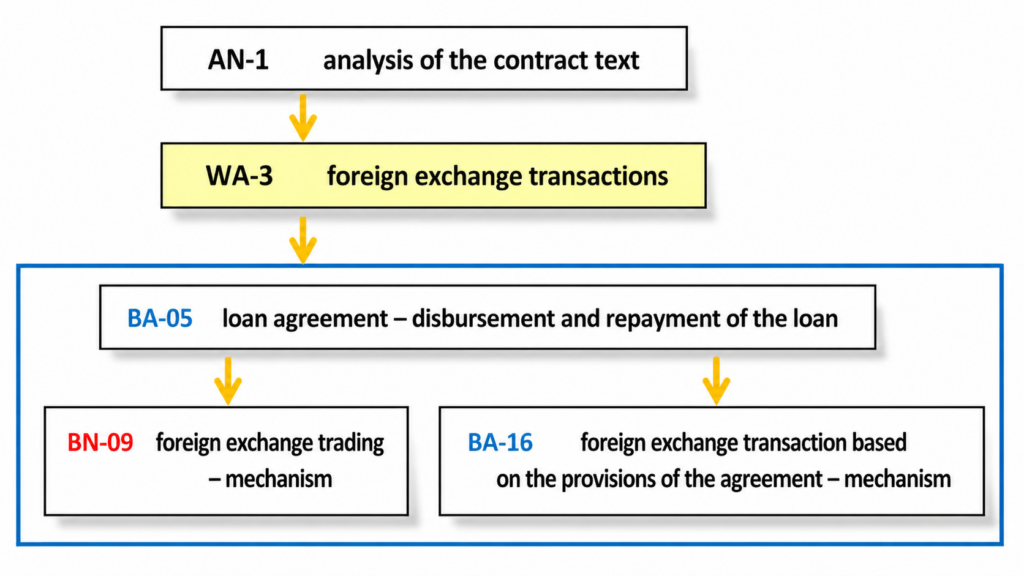

WA-3 currency trading in connection with the loan

In the case of dual-currency agreements, it appears as if, at the time of loan disbursement, banks were selling foreign currency, and at repayment they were buying it back.

In reality, there was not even any possibility of currency trading, because banks did not disburse the loan in foreign currency, and borrowers could not repay them in anything other than zlotys.

→ Let us nevertheless take a look at this “currency transaction”.

CONCLUSION

→ After comparing the mechanisms of currency trading and the operation based on the dual-currency agreement, the question — Is the disbursement and repayment of the loan connected with currency trading? — should be answered unequivocally:

one cannot sell currency using the buying rate and buy currency using the selling rate,

and yet this is what is written in the dual-currency agreement, so it was not currency trading but a transaction about which the average consumer had absolutely no idea. In accordance with the requirements of European law, the borrower should have been informed about this by loan advisers before signing the agreement. However, among hundreds of thousands of borrowers, not one heard what kind of transaction it was, which means that banks were violating the law on a massive scale.

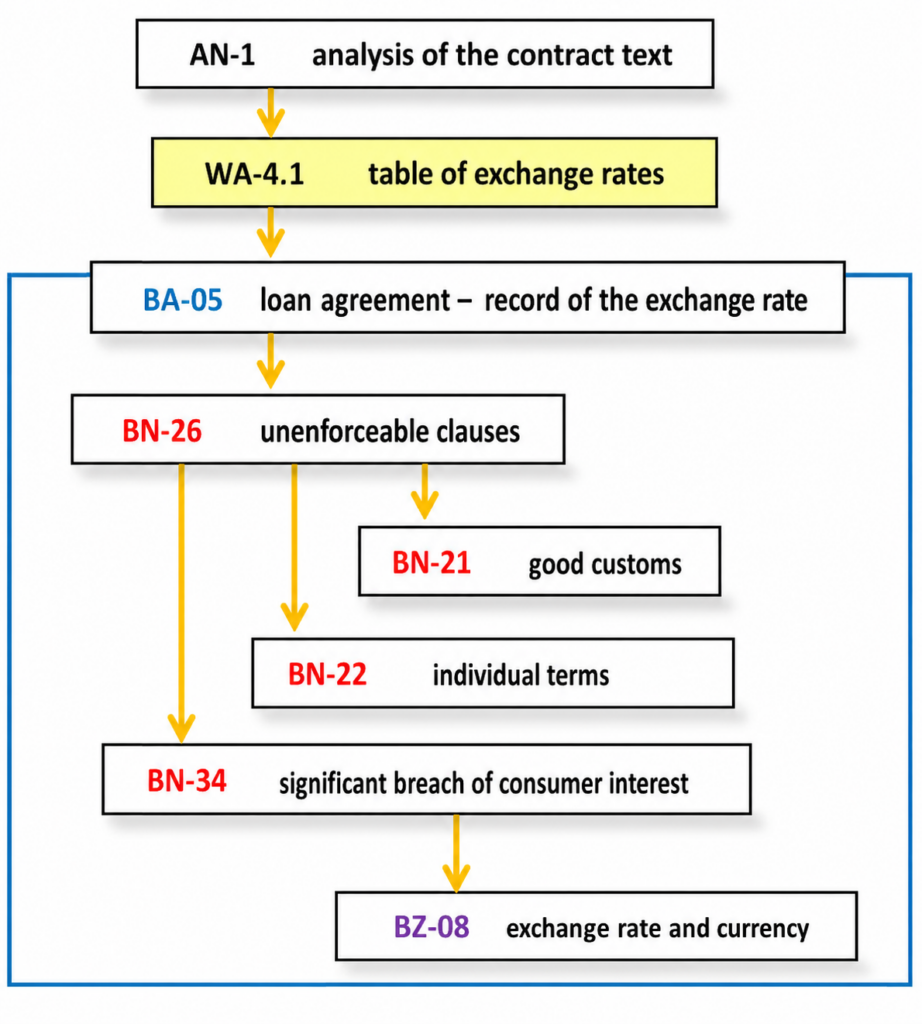

WA-4 the currency rate as an objective valorization indicator

The valorization indicator is the exchange rate, which should be an objectively determined indicator, i.e. independent of the will of either party to the agreement.

WA-4.1 → The lender’s currency selling-rate table as an objective valorization indicator?

Since banks have currency trading within the scope of their business activity and no one has ever questioned their right to determine their own currency prices, borrowers also accepted this clause almost automatically, although the repayment of a loan is no longer a one-off trade transaction in a currency exchange office but a long-term contract for the purchase of currency from one monopolist, namely our lender.

CONCLUSION

→ When a seller offers their product — e.g. a currency — on the free market, they may usually set the price freely, because no one has to buy from them or sell to them. However, in the case of dual-currency loan agreements, there was no free market, and it is impossible that bankers were unaware of this when drafting the agreements. Consumers may be unaware that currency trading and the granting of loans have entirely different natures. Banks guaranteed themselves the right to set the currency rate at the time of loan disbursement and repayment, which means

that market rights, i.e. the possibility of buying where it is cheaper and selling where it is more expensive, as well as the choice of when we want to carry out that transaction, do not apply here.

Mixing currency trading with a loan is contrary to logic and market rules.

The bank-lender, being a party to the agreement, secured for itself the exclusive right to set the valorization indicator, which is absolutely unacceptable.

It does not matter to what extent it exercised that right, i.e. how much it earned thanks to that clause.

This kind of regulation destroys the contractual balance between the bank and the consumer. Nothing else matters.

Even if the basic currency price is determined by the currency market, and the bank’s margin — constituting only a small part of it — does not significantly differ from the market average, the bank can still derive additional profit from the right to set the currency rate. Moreover, bankers wrote into the agreement “for 30 years you will pay as much as the market tells you to pay”, but earlier they calculated on which currency they would certainly not lose and might earn a lot! The currencies that banks chose for loan indexation could have significantly fallen against the Polish zloty only in the event of the end of the world. In other words, over a twenty- to thirty-year perspective, the probability of a significant fall in the rate of a foreign currency against the Polish zloty was close to zero, while the probability of a substantial rise exceeded 99%. Every currency-market analyst must have known this, although borrowers obviously did not have to. Does this not resemble usury?

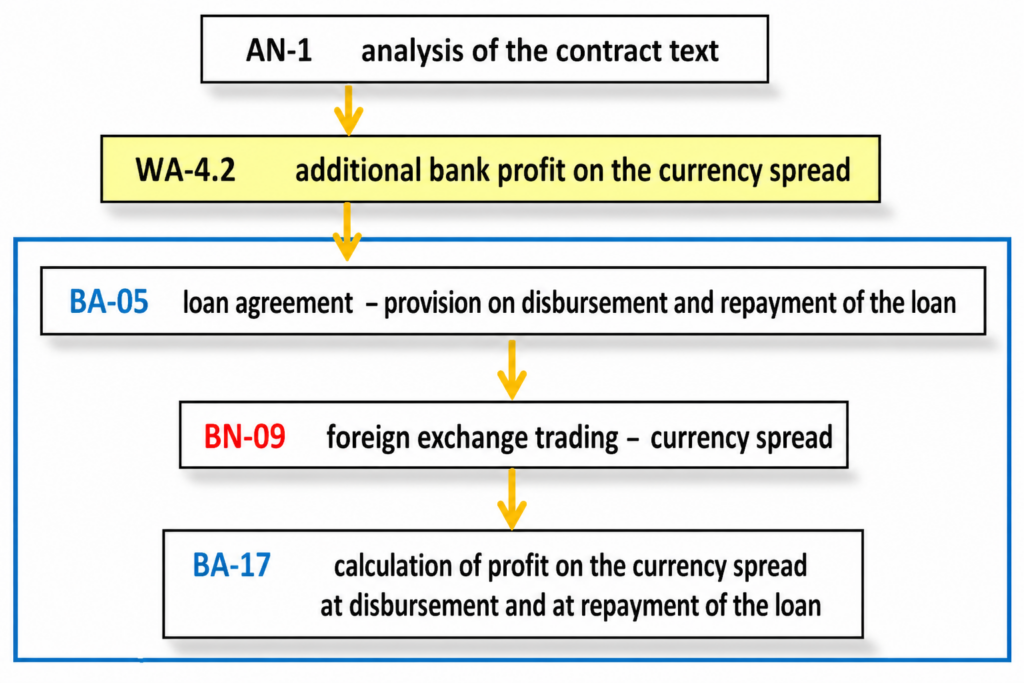

WA-4.2 profit on the dual-currency loan number 1 → currency spread

→ How much extra did the bank earn from the currency spread?

At the time of loan disbursement, banks converted the principal from one currency to another, and at repayment they converted it back again, each time earning on the difference between the buying and selling prices of currencies. Had they used the average NBP rate, there would have been no spread → let us calculate how much the bank earns on the spread.

CONCLUSION

In the case of dual-currency loans, banks offered a lower interest rate than for PLN loans, but they guaranteed themselves additional profit from the spread, which would have been impossible under a proper single-currency agreement!

And unfortunately, this is not the only additional profit of the bank under a dual-currency loan agreement. In a moment I will discuss the next profit-making mechanism added to the loan agreement without the borrower’s knowledge.

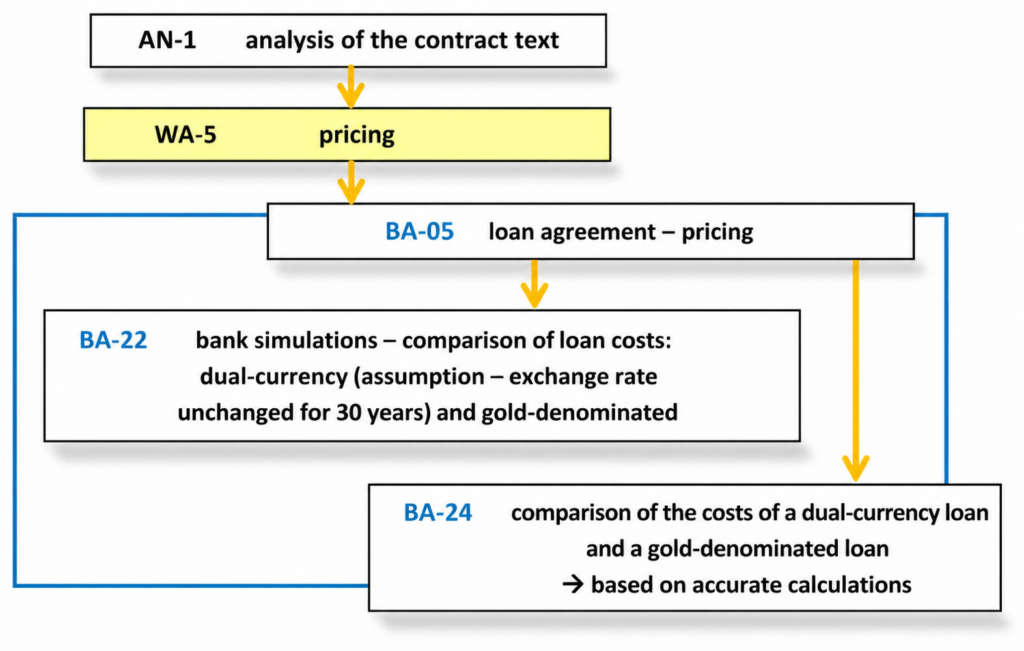

WA-5 profit on the dual-currency loan number 2 → interest + commission,

. . . . i.e. the only profit on a loan provided for by law (until 2011)

. . . . i.e. the only profit on a loan provided for by law (until 2011)

Interest and commission were the only loan-profit parameters provided for by law (until 2011). Interest should be the second most important element of the agreement — alongside the amount and the currency — on the basis of which every borrower decides whether they are able to repay the loan and whether they want to make use of that particular loan offer. This was the case until the appearance of dual-currency agreements, because those agreements disturbed the previous order.

CONCLUSION

Bank repayment simulations show that a PLN loan agreement and a dual-currency loan agreement differ only in interest, and this is contrary to the truth.

Once the correct parameters are used in the repayment calculation, it turns out that interest is not all that important here, because the lender secured for itself two other sources of profit in addition to interest, which are not provided for in the template of a loan agreement established by Polish regulations. The first of these additional loan-price parameters is the currency spread, which I have already discussed, and I will discuss the second in a moment.

Of course, interest is also one of the parameters of the price of this loan. It is not the most important element in the mechanism of earning on the loan, but interest still constitutes a significant source of income for the bank.

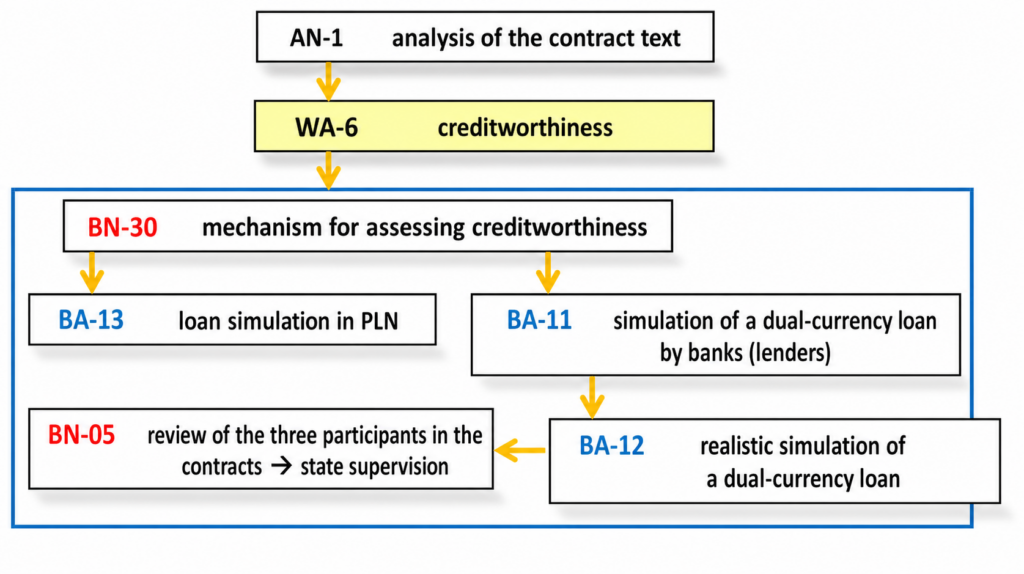

WA-6 creditworthiness

The examination of creditworthiness is carried out by the lender, and state supervision oversees it — or rather, should oversee it.

→ Does a properly conducted examination of creditworthiness show that a consumer working in Poland may have the capacity for a loan indexed or valorized to CHF, but not have the capacity for a PLN loan?

CONCLUSION

The repayment simulations for the dual-currency loan and the examination of creditworthiness were based on unrealistic assumptions.

A proper examination of creditworthiness shows that, in the long-term perspective, a PLN loan is cheaper than a dual-currency loan, and therefore the risk that the borrower will not repay it is lower.

However, the average Kowalski did not have to know that. Economists supervising that market should have known it. Did any state supervision of the consumer-loan market exist in Poland up to 2010? That is probably the only sensible question one can ask when analysing the dual-currency loan from this perspective.

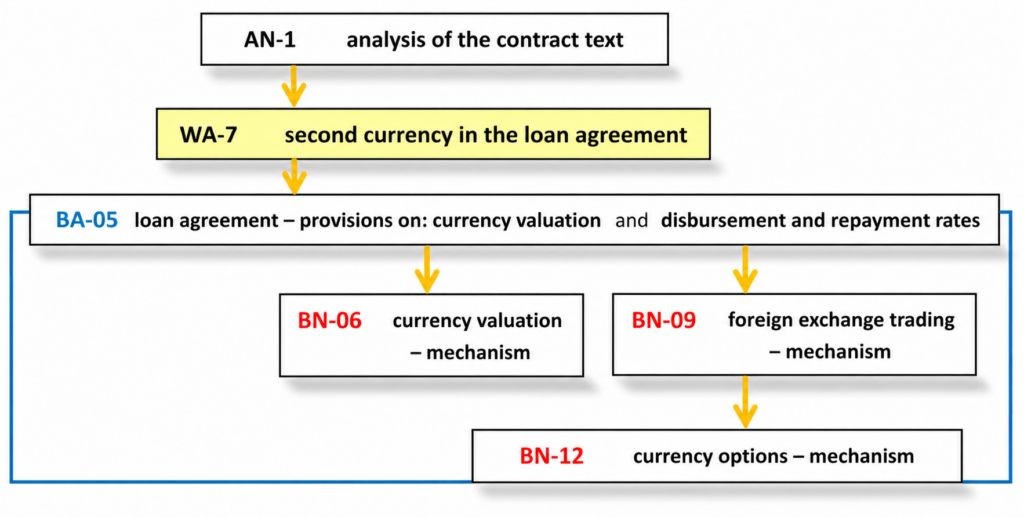

WA-7 profit on the dual-currency loan number 3 → currency options

Only now can we answer exhaustively the question: what was the second currency doing in the loan agreement?

And let me remind you that, under Polish Banking Law, it is a currency for which there is no place in a loan agreement!

Interesting why neither professors of law nor of economics have noticed that so far?

We already know that this second currency had nothing to do with valorization or with currency trading.

CONCLUSION

Entering the second currency into the agreement made it possible to offer an apparently lower loan price, i.e. a lower interest rate, and made it possible to add the sale of currency options in Swiss francs to the loan agreement.

The second currency is an ideal solution in two respects: marketing — it simulates more attractive loan conditions for the uninformed borrower, and also income-related — profit at least as high as on a PLN loan, and there is a huge chance (99%) that it will be muuuch higher if the borrower does not sell the currency options, or in other words, does not repay the loan before the CHF rate begins to rise sharply. The borrower, however, is convinced that they are repaying an ordinary loan and has 30 years to do so — they know nothing about any currency options — so why would they be in a hurry???

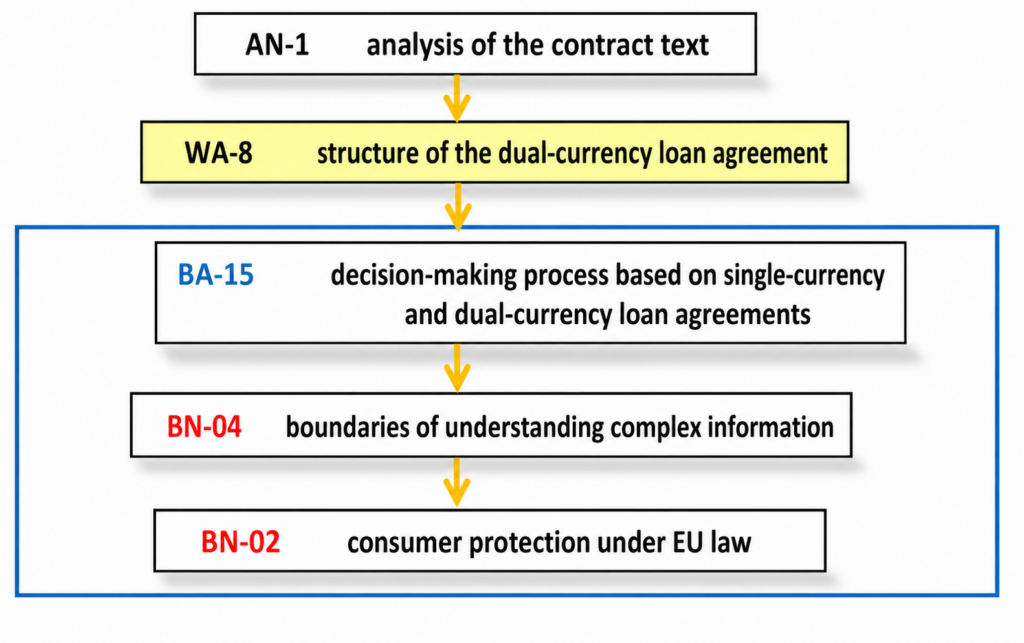

WA-8 structure of the dual-currency agreement

Only now can we answer the key question — could the content of this agreement have been understood by the average consumer?

→ We will compare the structure of single-currency agreements, i.e. in PLN and in a foreign currency [e.g. CHF], with the structure of a dual-currency agreement [e.g. indexed to CHF].

We will check whether the differences in their construction could have affected the decision-making process concerning the choice of loan type.

SUMMARY

Single-currency loan agreements have a simple structure in which the loan-price parameters most important to the borrower are clearly highlighted, because this is precisely how consumer agreements should look.

A PLN loan agreement requires one calculation — calculating interest on the borrowed principal.

A foreign-currency loan is just as simple, but one more factor appears — exchange-rate risk.

This risk can be quickly understood if one has the proper data on changes in the foreign-currency rate in the past!

However, it is impossible to understand the consequences of signing a PLN loan indexed (valorized) to a foreign currency without specialist knowledge.

The banks granting dual-currency loans cleverly added a second currency to the agreement in the form of valorization-indexation-denomination,

thus circumventing the regulations requiring the determination of the price of the loan in a specific currency, which enabled them to

change the mechanism of earning on the loan !!!

Instead of one loan-price parameter, namely interest, there are three price parameters here, because in addition there is the currency spread and currency options. Unfortunately, they are not clearly highlighted in the agreement. The elements necessary to calculate the price of the loan are hidden in many paragraphs, and assembling these puzzles into one whole is entirely impossible for the average consumer.

The only visible parameter of the loan price is the interest rate, but here it actually serves as a marketing lure, because the principal price of the loan is shaped by the rules of trading in currency options, which so far have not been noticed by the economic community (including professors, university rectors and presidents of the NBP) taking part in the debate on pseudo-currency loans.